Jahangir's World Times First Comprehensive Magazine for students/teachers of competitive exams and general readers as well.

Jahangir's World Times First Comprehensive Magazine for students/teachers of competitive exams and general readers as well.

Attributes of A Good Tax System

Bilal Hassan

Fundamentally, every government plans its monetary and fiscal policies to achieve higher economic growth, i.e. GDP, to keep inflation in check and to curtail unemployment rates. On the fiscal front, governments make efforts to maximize their revenues so as to avoid fiscal deficit which is considered harmful to the society due to its increasing impact on the prices of goods and services. In today’s world, almost all countries raise their revenues through taxes. Taxes whether direct or indirect affect one or more components of the growth equation — consumption, investment, expenditure, imports and exports. In advanced economies, efforts are being made to enforce a tax system that does not hurt the economic growth on the one hand, and increases tax revenues, on the other. This article provides attributes of a good tax system that accelerates economic growth and optimizes tax revenue.

Fiscal Adequacy

A government has to make payments for goods and services. To meet its expenditure, it requires sufficient funds in continuous flow. Tax revenue and non-tax revenue are major sources of funds for the governments for balancing budgets. Besides, the governments can borrow money from foreign and domestic donors in case revenues fall short of expenditures in a fiscal year. A tax is, therefore, said to be good if it:

- generates adequate revenue to enable the government to meet its budgetary needs without resorting to deficit financing;

- keeps up revenue growth with the pace of economic growth in the long run, which is essential for the policymakers to devise revenue-related futuristic policies; and

- is a stable tax in terms of tax base, tax rate and tax administration. Stability is fundamental to effective planning and efficient compliance.

Simplicity

A tax must be so simple that its provisions are easily understandable. A simple tax is required, inter alia, to:

- reduce cost of tax collection on tax authorities;

- make its compliance easier for taxable persons;

- minimize cost of tax compliance to taxable persons;

- minimize risks to businesses; and

- allow taxable persons to claim their rights (statutory deductions, tax refunds, tax credits, etc.) without any ambiguity.

A tax becomes simple when its legislation has:

- minimum tax exemptions and tax concessions because besides revenue losses directly, these have the impact of squeezing the tax base, and shifting the burden onto a smaller number of existing taxable persons so as to compensate for the loss of revenue;

- no special schemes for designated sectors of economy as it is essential to prevent tax fraud and tax evasion. It is empirically quantified that concessionary regimes and special schemes reduce VAT compliance and increase tax evasion;

- not too many tax rates because multiple rates are associated with higher administrative and compliance costs and tend to reduce VAT efficiency; and

- clear tax provisions to enable taxable persons to claim their rights without undergoing prolonged litigation.

Neutrality

To promote economic growth and to achieve economic efficiency, it is fundamental that governmental interventions in the economy should be the minimum, or at least its policies must not change the behaviour of the economic agents – consumers, investors, importers and exporters, etc. In other words, its actions must be neutral to economy. As governments raise tax revenue, taxes may modify the behaviour of economic agents and may reduce efficiency and productivity of an economic system. A tax is said to be good if it remains neutral between forms of business activities. A neutral tax does not interfere with the allocation of resources and its application does not modify the decisions of consumers and investors concerning consumption and investment. Moreover, a neutral tax leaves production undistorted, according to production efficiency theorem by Diamond and Mirrlees (1971). A neutral tax thus helps in:

To promote economic growth and to achieve economic efficiency, it is fundamental that governmental interventions in the economy should be the minimum, or at least its policies must not change the behaviour of the economic agents – consumers, investors, importers and exporters, etc. In other words, its actions must be neutral to economy. As governments raise tax revenue, taxes may modify the behaviour of economic agents and may reduce efficiency and productivity of an economic system. A tax is said to be good if it remains neutral between forms of business activities. A neutral tax does not interfere with the allocation of resources and its application does not modify the decisions of consumers and investors concerning consumption and investment. Moreover, a neutral tax leaves production undistorted, according to production efficiency theorem by Diamond and Mirrlees (1971). A neutral tax thus helps in:

- achieving broader tax base;

- taxing broader base at lower rates;

- optimizing tax revenue;

- enhancing economic productivity; and

- stabilizing the economy.

Efficiency and Effectiveness

An efficient tax yields maximum tax revenue with minimum costs. An efficient tax:

- imposes less administrative cost on tax authorities;

- entails less compliance cost on taxable persons; and

- yields more revenue.

A good tax should produce the right amount of tax at the right time. A tax is said to be effective if it minimizes the potential for tax evasion, tax fraud and tax avoidance.

Equity

Two measures of equity include:

- horizontal equity that requires taxable persons with equal level of income pay the same amount of tax and thus bear equal tax burden. Horizontal equity is essential for fairness and for improving compliance level; and

- vertical equity requires taxable persons with different levels of income should pay different amounts as tax and thus bear unequal tax burden. In other words, taxable persons with high income level should pay higher taxes as a percentage of their income than those taxable persons having comparatively less income. Thus, vertical equity is essential for distribution of wealth and reducing income inequalities.

By maintaining horizontal and vertical equity and besides generating adequate revenue, a good tax seeks to achieve redistribution of wealth from the rich to the poorer segment of the society and thus minimizes income inequalities within the society.

Exportability and adjustability

An exportable tax is the one that is at least partially paid by the nonresidents who use a state’s transportation infrastructure. There are broadly three ways in which taxes can be exported: by having non-residents pay the tax directly; by levying taxes on businesses which are then passed on to non-residents; and through interaction with the federal income tax.

Moreover, a good tax must be border-adjustable, i.e., all domestic supplies in a country with a border-adjusted tax pay the same amount of tax regardless of country of origin. Second, in the global market, a border-adjusted tax places exports on an equal footing with products from other countries because they will all face the same amount of tax regardless of where they are sold.

After brief discussion on attributes of a good tax, this article highlights attributes of a good tax. Research questions why VAT is said to be good tax and whether VAT is always a good tax are being analyzed thereafter.

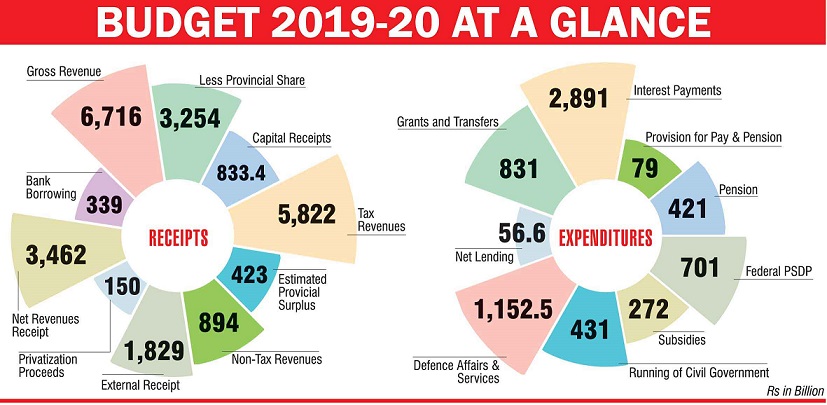

What is Fiscal Deficit?

The difference between total revenue and total expenditure of the government is termed as fiscal deficit. It is an indication of the total borrowings needed by the government. While calculating the total revenue, borrowings are not included.

The gross fiscal deficit (GFD) is the excess of total expenditure including loans net of recovery over revenue receipts (including external grants) and non-debt capital receipts. The net fiscal deficit is the gross fiscal deficit less net lending of the Central government.

Generally fiscal deficit takes place either due to revenue deficit or a major hike in capital expenditure. Capital expenditure is incurred to create long-term assets such as factories, buildings and other development.

A deficit is usually financed through borrowing from either the central bank of the country or raising money from capital markets by issuing different instruments like treasury bills and bonds.

{kind=link}