Jahangir's World Times First Comprehensive Magazine for students/teachers of competitive exams and general readers as well.

Jahangir's World Times First Comprehensive Magazine for students/teachers of competitive exams and general readers as well.

US-China Trade War and Global Economy

The longer the war continues, the greater the risk of de-globalization becomes

Shafqat Javed

Recently acting IMF Managing Director, David Lipton, in a veiled appeal, called on the United States and China to come to an agreement and end their yearlong trade war by saying that the global economic slowdown has been “certainly affected by the trade tensions,” though he did not mention the US or China by name. Citing that global trade has been lower in the first six months of the current year compared with the same period in 2018, he said that it’s “time for vigilance … It’s time for the countries to have dialogue, to reach agreements, to try to find a way through this, since the global economy is fragile.” And this apprehension seems to get materialized as President Trump’s threat to put 10 percent tariffs on the remaining $300 billion of Chinese imports that aren’t subject to his existing levies sent markets tumbling from Asia to Europe and in the US.

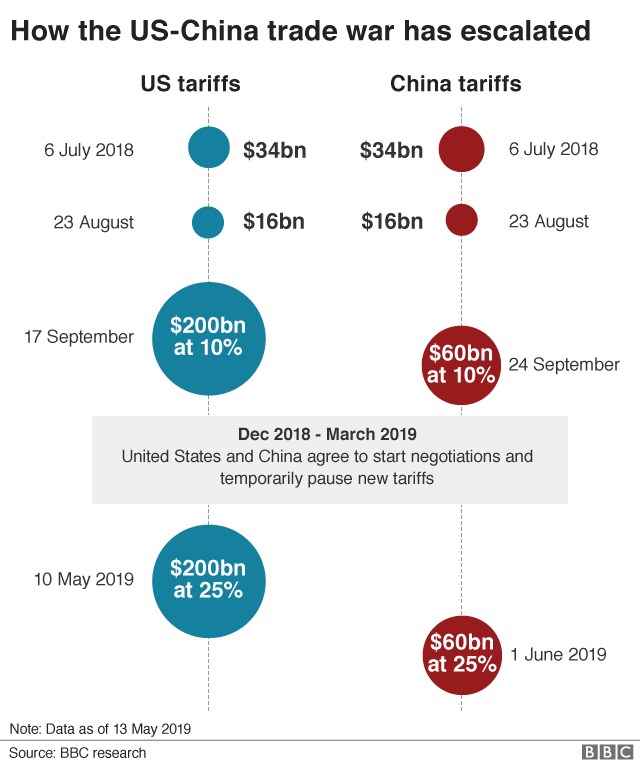

Although US President Donald Trump and Chinese President Xi Jinping agreed at the G20 summit in Osaka to resume trade negotiations, the path to ending the trade war remains far from clear. Recently, after the latest round of bilateral talks showed little sign of a breakthrough, President Trump announced to impose a fresh 10 percent tariff on another $300bn of Chinese goods; effecting another sharp escalation of a trade war between the two countries that is all set to hurt the global economy.

The US Chamber of Commerce, which represents more than three million US companies, said the latest tariffs on China “will only inflict greater pain on American businesses, farmers, workers and consumers, and undermine an otherwise strong US economy”. Mr Trump says his trade tactics are working, and that Beijing is feeling the pain. But China isn’t the only country that is gett8ing hurt; the International Monetary Fund, too, has warned that the US-China trade war is the biggest risk to the global economy. And, there is mounting evidence to show it’s also hitting the American economy which grew less than previously thought last year. The figures showed foreign trade and business investment shrank as the trade war wore on. US firms are holding off on expansion plans and investments, meaning new factories aren’t being built and new jobs aren’t being created.

The US Chamber of Commerce, which represents more than three million US companies, said the latest tariffs on China “will only inflict greater pain on American businesses, farmers, workers and consumers, and undermine an otherwise strong US economy”. Mr Trump says his trade tactics are working, and that Beijing is feeling the pain. But China isn’t the only country that is gett8ing hurt; the International Monetary Fund, too, has warned that the US-China trade war is the biggest risk to the global economy. And, there is mounting evidence to show it’s also hitting the American economy which grew less than previously thought last year. The figures showed foreign trade and business investment shrank as the trade war wore on. US firms are holding off on expansion plans and investments, meaning new factories aren’t being built and new jobs aren’t being created.

But, despite several rounds of talks, the world’s two largest economies have failed to reach an agreement to end the trade war rather the tensions have intensified owing to which global growth prospects seem bleak as they slowly but surely have moved from the ideal and preferable scenarios towards the worst and darkest.

In the first scenario, a return to cooperation, the US and China achieve a trade agreement. Both agree to phase out additional tariffs, renounce trade threats and establish working groups to defuse other friction areas in intellectual property rights, social and political issues, and military matters.

Global growth prospects could — in the best scenario — exceed the old baselines of the Organisation for Economic Cooperation and Development or the International Monetary Fund, at more than 4 per cent.

This was always the least likely scenario and, today, its probability is minimal. Yet, it is important to remember that around the time of the first meeting in 2017 between US President Donald Trump and Chinese President Xi Jinping, many observers saw the scenario as possible, even probable.

In the second scenario of muddling through, the tariffs’ economic impact is limited to 0.4 per cent of China’s economy and 0.8 per cent for the US. During the truce, the US and China develop a path to a trade agreement but other friction areas, particularly in advanced technology, result in new skirmishes.

Uncertainty decreases but fluctuates. Global economic prospects barely improve. Markets witness rallies and plunges. Global recovery fails. Global growth prospects remain close to 3.5-3.9 per cent. Only half a year ago, this scenario was still seen as viable. Today, it feels like a bygone world.

In the third, America First, scenario, the import value at stake is tenfold relative to the start of the trade war, amounting to more than US$500 billion, with soaring collateral damage. In China, it could shave 0.4 per cent off economic growth this year and, in the US, 0.8 per cent. Neither the US nor China agree to phase out additional tariffs. Talks linger, fail or lead to new friction.

In the third, America First, scenario, the import value at stake is tenfold relative to the start of the trade war, amounting to more than US$500 billion, with soaring collateral damage. In China, it could shave 0.4 per cent off economic growth this year and, in the US, 0.8 per cent. Neither the US nor China agree to phase out additional tariffs. Talks linger, fail or lead to new friction.

Uncertainty increases, volatility returns. Global prospects decline further. Markets linger at the depths. In this scenario, global prospects dampen as world economic growth in 2019 sinks to 3 per cent or worse.

Finally, in the scenario of a global trade war, all bets are off. The US and China fail to agree on a compromise. Additional tariffs are enacted and new trade threats declared. The White House escalates attacks against Chinese industries, taking aim at intellectual property rights, social and political issues, and military modernisation. Volatility soars. Real economic growth in the US takes a severe hit. Chinese growth erodes.

Eventually, risks to the global outlook overshadow world economic growth, which could linger at 2-2.5 per cent or worse. World trade and investment plunges. Migration crises abound. The number of globally displaced, which has exceeded World War II figures since the mid-2010s, soars to record highs. A series of new geopolitical conflicts prove harder to contain.

So, where are we today with regard to these scenarios? A simple answer is: moving closer to the edge. After trade frictions and the Trump tariffs undermined the momentum of global recovery, the International Monetary Fund finally woke up to the effects and started predicting that global economic activity will slow notably.

In early June, the World Bank estimated the world economy would expand by only 2.6 per cent. The IMF has also warned that trade wars could wipe US$455 billion off the world’s gross domestic product in 2020. Worse, Trump increased tariffs on US$200 billion worth of Chinese goods exported to the US, and introduced an effective ban on American companies doing business with Chinese telecom giant Huawei Technologies in May.

In brief, the status quo is shifting from the America First scenario towards an all-out global trade war.

In effect, multilateral banks’ estimates are still downplaying the collateral damage. If the Trump administration continues to expand trade wars and geopolitical ploys in multiple regions, their models ignore the impending adverse feedback of such measures — as evidenced by Morgan Stanley’s business conditions index that just took the worst one-month hit in its history.

To understand how much expectations have been revised, recall that before the 2008 crisis, the global growth rate was 4-4.3 per cent. The current rate has almost halved from its pre-crisis level. Something similar occurred in the 1970s, which saw the end of the “glorious 30” — three decades of solid post-war growth in major advanced economies.

What we are witnessing now is a potentially fatal fall into long-term stagnation. In part, it is structural, resulting from maturing economies and ageing populations. But, in part, it is self-induced and the effect of misguided trade policies and unilateral geopolitical aggression. In the absence of tariff wars and geopolitical destabilisation, the global growth rate could now be closer to 3.5 per cent.

The longer it takes to achieve multilateral reconciliation, the more likely it is that falling long-term growth rates will prove harder to reverse.

Will Trump’s Trade Wars Reshape the Global Economy?

A trade war between the United States and China that began last year appeared to be inching toward a conclusion recently, but only after bringing the world to the brink of a global trade crisis and damaging producers—particularly US farmers. Trump launched the trade war over China’s perceived unfair trade practices, including forced technology transfers and the theft of intellectual property. Now negotiations have once again stalled, and Trump has returned to the threat of raising tariffs on a broad range of Chinese imports to the US

A trade war between the United States and China that began last year appeared to be inching toward a conclusion recently, but only after bringing the world to the brink of a global trade crisis and damaging producers—particularly US farmers. Trump launched the trade war over China’s perceived unfair trade practices, including forced technology transfers and the theft of intellectual property. Now negotiations have once again stalled, and Trump has returned to the threat of raising tariffs on a broad range of Chinese imports to the US

That may be particularly concerning to European officials who are set to start their own trade negotiations with the US Trump has already decried what he sees as unfair trade deficits with European Union countries, particularly Germany, and he imposed tariffs on steel and aluminum imports from some allies, without seeming to understand that the EU negotiates trade terms as a bloc. A US-Europe trade war could do lasting damage to both sides.

Trump’s one clear-cut accomplishment on trade is the updated NAFTA deal known officially as the US-Mexico-Canada Act, or USMCA. But it mainly recoups the self-inflicted losses from Trump’s withdrawal from the Trans-Pacific Partnership trade deal—only on a smaller North American, rather than trans-Pacific, scale. If that weren’t bad enough, the jury is still out on whether the deal will manage to survive ratification in the US

It does not help that with the global economic trade system in flux, the body charged with overseeing it is in crisis, exacerbated by the Trump administration’s hostility to multilateral institutions of all stripes. Trump has accused the World Trade Organization of violating US sovereignty, and his administration seems intent on hobbling it due to practices Trump perceives as unfair to the US Though the WTO is clearly in need of reforms, Trump might opt to sink the body rather than try to fix it.

{kind=link}